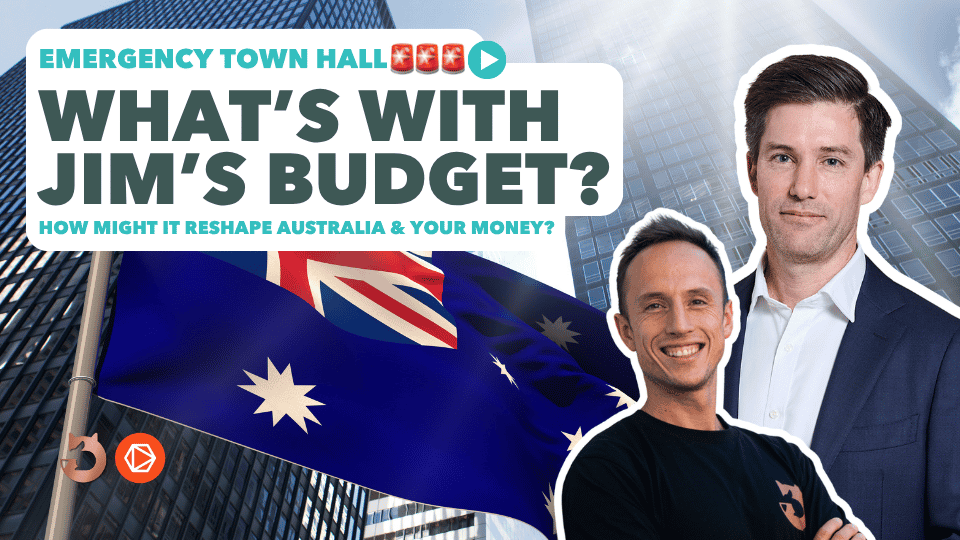

Mission-Critical or Media Noise?

Financial freedom should be defined by your strategy, not the changing whims of the political cycle.

Last week, however, Treasurer Jim Chalmers handed down a budget that sent the nation into a tailspin, with proposed changes to Capital Gains Tax and Negative Gearing dominating every headline.

If you felt a spike of uncertainty about your long-term wealth and wealth building strategy, you weren’t alone.

In our latest Emergency Town Hall, Co-founder Glen Hare and BetaShares Senior Strategist Cam Gleeson sat down to separate fact from friction.

They broke down the three major policy pillars currently under debate and, more importantly, explored options for keeping portfolios flexible and ‘future-proof moving forward.

Watch the video briefing or read the article below!

In Short:

📉 CGT Overhaul: The 50% discount is on the chopping block, proposed to be replaced by an indexation model that could change how you build long-term wealth.

🏠 Negative Gearing: New restrictions aim to push investors toward new builds, though existing properties are expected to be grandfathered.

🤝 Trust Tax Floor: A proposed 30% minimum tax on distributions aims to close loopholes for family trusts and small businesses.

🛡️ Stay the Course: These changes aren’t slated until July 2027, giving us plenty of time to refine your strategy before anything is set in stone.

Your Next Step:

Get the facts by reading the breakdown or watching the session below. Remember, we have time on our side—nothing is set in stone until 2027. If you have specific questions about your current strategy, record your questions and save them until your strategic review.

1. The CGT Overhaul: Turning Back the Clock

The headline act of the budget was a total rewrite of how we tax profit. For over 20 years, Australian investors have relied on a simple 50% discount—if you held an asset for more than a year, the government only taxed half the gain.

Now, the government is proposing to scrap that discount and replace it with an Indexation model plus a 30% tax floor.

But what does that actually mean?

Instead of a flat discount, your original purchase price would be adjusted in line with inflation. You would only pay tax on the “real” gain—the growth that actually outpaced the cost of living.

Jim’s proposed “indexation” model hits the rewind button to 1999, swapping the 50% discount for a system that only taxes gains above inflation. Cam says it’s a move toward a “purer” economic model but potentially adds a massive compliance burden for everyday investors.

The “Trojan Horse” Warning

While much of the pre-budget talk focused on property, Cam highlighted that this change is a bit of a “Trojan Horse”. What started as a housing fix has expanded to capture almost every asset class, including your ETFs and shares.

The Fox & Hare Reality Check:

✅ The Pro:

It’s a “purer” economic model because it ensures you aren’t paying tax on inflation.

❌ The Con:

Cam warned that this adds “immense compliance costs” and could lead to a “lock-in effect” where investors refuse to sell assets because the tax burden feels too high.

👩⚖️ The Verdict:

Cam described this as a “backward step” for tax simplicity. It potentially discourages the long-term compounding that young professionals need to build wealth and get on the property ladder.

Missed the whole session? Hit the image, plug in your headphones and get up to speed.

2. Negative Gearing: Shifting the Goalposts

Negative gearing is easily one of the most “emotional” topic in Australian finance.

It’s been the engine room for property investors for decades, but the budget signals a major change in direction: the government wants to limit these tax deductions strictly to new builds.

Construction over Speculation

The Treasurer’s argument is straightforward – he wants to push private capital away from “speculating” on existing apartments and toward the creation of new housing stock.

The goal is to solve the supply crisis by incentivising construction

The Grandfathering Clause

If you already own an investment property, you can breathe a little easier, though.

The current proposal includes “grandfathering,” meaning that your existing arrangements are expected to stay exactly as they are. However, as Cam noted, this could create two very different classes of investment property in the future.

The Fox & Hare Reality Check:

📉 The Supply Risk:

Critics argue that if investors stop buying established homes, the rental supply could contract sharply, driving up rents for those who can least afford it.

🏆 Quality First:

Glen’s position was clear: “Tax is an outcome”. Saving a few thousand dollars a year on tax is pointless if you’re holding a low-quality asset that isn’t growing in value. Focus on investing wisely rather saving pennies.

⚖️ The Bottom Line:

Don’t let the tax tail wag the investment dog. Whether it’s a new build or established, the asset quality and performance must come first.

The goalposts have shifted, but Glen’s thinking hasn’t: “Tax is an outcome.” He says. Whether it’s a new build or a heritage terrace, the asset’s growth potential should always matter more than the tax deduction.

3. The Trust Tax Floor: Closing the “Loophole”

The third major change discussed was a proposed 30% minimum tax floor on distributions from discretionary trusts.

Many families use trusts to distribute income strategically. By moving funds to the member with the lower income, they actively reduce the amount of tax the household pays as a whole.

The government is now positioning these trusts as a “loophole” that needs to be closed.

What are the proposed changes?

Under the proposal, any distribution from a discretionary trust would be subject to a minimum tax rate of 30%. For those currently distributing to family members who fall below that tax bracket, this could lead to a significant increase in the annual tax bill.

The Fox & Hare Reality Check:

🏢Small Business Impact:

Critics argue that because discretionary trusts are the standard vehicle for many farmers and small businesses, this flat tax will act as a penalty on “working capital”—making it harder for businesses to reinvest in their own growth.

📋 Complex Administration:

As Glen noted, trusts are already expensive to set up and administer. This change adds another layer of complexity to a structure that was already only appropriate for a specific slice of the population.

⚖️ The “Level Playing Field”:

While it’s a tough pill to swallow for some, Cam noted that from a policy perspective, this is being framed as an attempt to “level the playing field” so that capital isn’t consistently taxed at a lower rate than standard salary income.

💡 The Bottom Line:

If you currently operate through a trust, this is the time to review your structure. Unwinding or adjusting a trust is possible, but it’s a significant move that requires expert guidance. Of course, legislation has not yet passed!

The proposed 30% tax floor is a direct challenge to one of the most common tax reduction strategies: income splitting. By setting a minimum rate, the government aims to ensure family wealth is taxed more like a standard salary, effectively closing what they call a loophole allowing those with access to a trust to minimise their tax contributions.

4. Opportunities & Strategies: Making Change Work for You

With every budget comes a set of new rules—and with every new rule, there is a potential for a new strategy.

During the webinar, Glen and Cam shifted the focus from “what we’re losing” to “how we can stay efficient.”

Finding the “Indexation Winners”

Under the proposed indexation model, assets that generate more of their return through income rather than massive capital gains (like fixed-income bonds or certain Australian shares) may actually see better after-tax outcomes than they did under the old 50% discount system.

The ETF Edge

Exchange Traded Funds (ETFs) have always been a staple of efficient portfolios, but their structure might become even more valuable if these CGT changes stick. Because ETFs generally have lower turnover than unlisted managed funds, they can delay the CGT “hit” until you actually decide to sell.

By controlling the timing, you may be able to keep more of your money working for you in the market rather than paying it out to the ATO every year.

The “Safe Harbour” of Super

Despite all the noise, the budget papers explicitly carved out superannuation, suggesting it remains an untouched “safe harbour.”

Depending on your life stage, it may make sense to adjust your asset mix—perhaps tilting toward capital growth within the tax-advantaged environment of super, while keeping more income-oriented or defensive assets outside of it.

The Fox & Hare Reality Check:

🌍 Stay Diversified:

Even if certain tax benefits change, global diversification remains the single best tool for wealth accumulation. Don’t let a local tax change stop you from accessing the growth of the world’s best markets.

🛡️ Avoid the “Debt Trap”:

Glen called out margin loans specifically. With interest rates sitting around 10%, you need your underlying assets to perform exceptionally well just to break even. In a high-tax environment, the math for margin lending gets even tougher.

⚡ Look for Efficiency:

Cam noted that internally geared ETFs (with interest rates closer to 5%) are a far more cost-effective alternative to traditional margin loans.

⚖️ The Bottom Line:

Strategy beats speculation. Regardless of the tax environment, your investment vehicle and asset quality should always come first.

New rules don’t mean the end of growth; they just require a new map. From the structural efficiency of ETFs to the “safe harbour” of Super, we’re always working hard to identify the vehicles that keep your money working for you.

Audience Questions Answered

We had some great questions come through during the session. Read on to get Glen and Cam’s perspectives:

🛡️ Sarah asked:

“Is there any suggestion that the current CGT exemptions on education bonds after the 10-year mark will change?”

The Answer:

We haven’t seen any indication that these will be affected. Given that superannuation was explicitly “carved out” and protected, it’s likely that investment and education bonds will remain a “safe harbor” for tax-efficient growth.

💡 Vineet asked:

“What was the government’s thinking in applying CGT changes to non-property investments like the stock market?”

The Answer:

Cam described this as a “Trojan Horse” strategy. While the conversation started around property, the policy was expanded to capture all capital assets. The overarching philosophy appears to be an attempt to ensure that capital gains are taxed at a minimum of 30%, aligning them more closely with standard salary tax rates.

♻️ Gavin asked:

“Do the negative gearing changes have any implications for the use of debt recycling from my home?”

The Answer:

If you recycle debt to invest in shares or ETFs, the interest remains tax-deductible under the current proposals. However, if you use that equity to purchase an existing investment dwelling, that interest would likely no longer be tax-deductible.

📉 George asked:

“Is there any benefit to using margin loans to navigate these changes?”

The Answer:

At current interest rates of roughly 10%, margin loans are an expensive play. Because indexation is more punitive on high capital gains, you’d need your underlying asset to perform exceptionally well just to break even. For most, this makes margin loans a high-risk, low-reward option in the current environment.

Eyes on the Prize – Always

As you can see, there’s a lot of complexity to unpack here, and much of it will remain fluid until these proposals are officially legislated (or shot down in parliament).

If you’re feeling unsure about how your current portfolio stacks up against these potential changes, please don’t stress – reach out to your team via the Personal Finance Portal to find out when your next strategic review is scheduled.

High-achieving, experienced, and always in your corner. Your Fox & Hare advice team are always working to ensure you are in the best possible possible position – please reach out via the PFP with any questions!

About Fox & Hare:

Fox & Hare are the Millennial and Gen Z advisers, 100% focused on helping Australia’s 20-45 year olds buy property, get invested and achieve financial freedom.

When it comes to managing your money, it’s normal to feel uncertain or scared of making the wrong decision; it’s normal to feel so overwhelmed that, despite knowing you need to do something, the first step seems impossible; and it’s also incredibly normal to be earning great coin, but still feeling like you’re behind.

At Fox & Hare we create bespoke, long term financial plans that eliminate these uncertainties and put you in control of your financial future. No more option paralysis. No more fear of missing out. No more uncertainty about how to manage your money effectively.

If you:

- Want to achieve financial freedom.

- Want the flexibility to live your life on your terms, not tied to a job or working 24/7.

- Want your money to be working for you – not the other way around.

But the idea of learning how and where to start is more than a little daunting, let Fox & Hare do the legwork for you.

Read more insights from our experts

Interior Design Decoded: Your Framework for a Beautiful, Functional Home.

The Cost vs. The Joy of Living Australia is a nation of property addicts. We talk about buying property, we talk about renting...

From Big Firms to Big Dreams: How Maira Engineered Her Corporate Exit.

The architecture of financial freedom. In short: Walking away from a secure income is terrifying, especially with a family and a mortgage – but...

What’s Donald Doing in Iran?

Stormy Seas Ahead? Recently, Fox & Hare Co-founder Glen Hare caught up with Hugh Lam, Investment Strategist at BetaShares, to discuss the escalating situation...

Your Membership has Changed: What’s New & How Will You Benefit?

Our memberships have changed! Recently, Fox & Hare made the most significant changes to our ongoing membership structures since the business’s inception. To ensure our...

A Divorce, a Resignation Letter, and a Boarding Pass: The Art of Starting Over (in NYC🗽)

What do you do when the world falls apart? In short: Facing a divorce, career pivot and global pandemic head on, Danica did what...